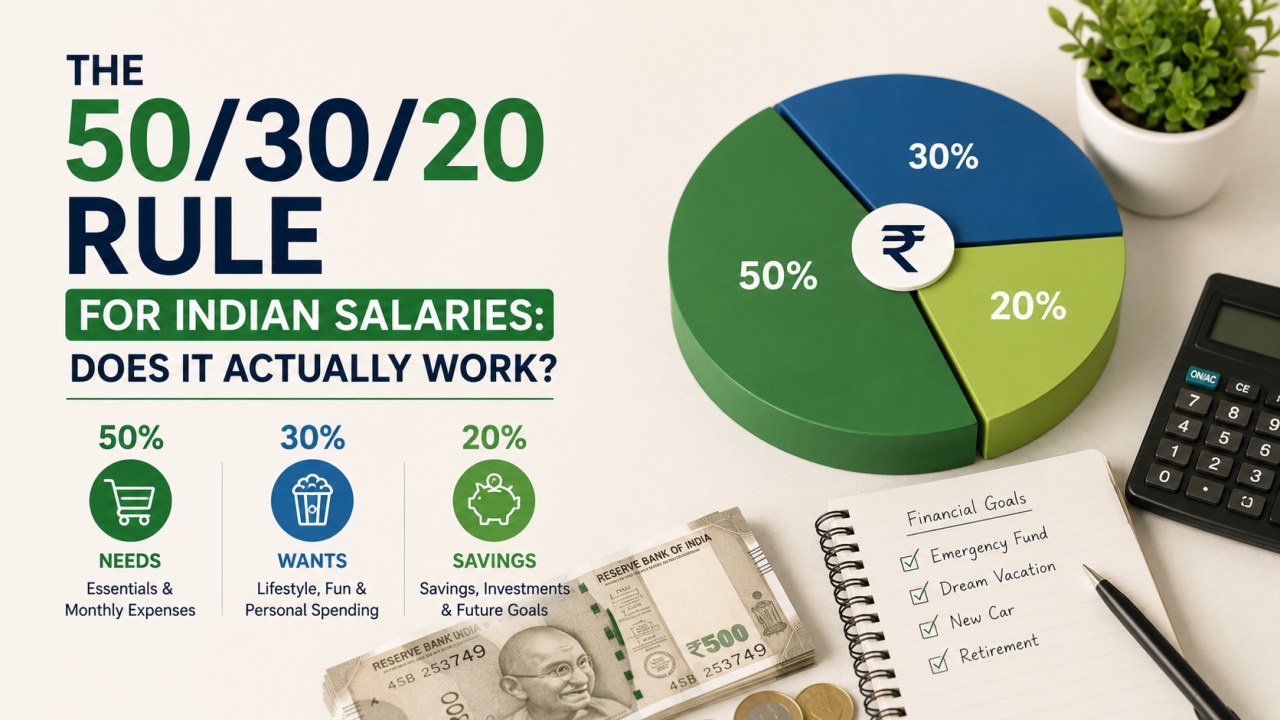

The 50/30/20 rule says: spend 50% of your monthly take-home on needs, 30% on wants, save the remaining 20%.

It was made famous in the US by Senator Elizabeth Warren. It's the most-cited personal finance framework on the internet. And in Indian cities, it usually doesn't fit out of the box.

This article runs the rule through real Indian numbers and shows when to adjust.

The original 50/30/20 in plain ₹

For a take-home of ₹50,000 / month:

- ₹25,000 (50%) — Needs: rent, food, EMI, utility bills, basic transport, insurance premiums

- ₹15,000 (30%) — Wants: eating out, OTT, weekend trips, shopping

- ₹10,000 (20%) — Savings & investments: SIP, emergency fund, PPF, retirement

Sounds clean. Then you live in Bengaluru and your 1BHK rent is ₹28,000.

Where the rule breaks in Indian cities

The maths is unforgiving:

| City | Typical 1BHK rent | Avg take-home for ₹50–80k earner | Needs % consumed by rent alone |

|---|---|---|---|

| Mumbai (Andheri/Powai) | ₹30,000 – ₹45,000 | ₹65,000 | 46% – 69% |

| Bengaluru (Koramangala/Indiranagar) | ₹25,000 – ₹40,000 | ₹70,000 | 36% – 57% |

| Delhi NCR (South Delhi/Gurgaon) | ₹20,000 – ₹35,000 | ₹65,000 | 31% – 54% |

| Pune | ₹18,000 – ₹28,000 | ₹55,000 | 33% – 51% |

| Hyderabad | ₹15,000 – ₹25,000 | ₹55,000 | 27% – 45% |

| Tier-2 (Indore, Jaipur, Coimbatore) | ₹8,000 – ₹15,000 | ₹40,000 | 20% – 38% |

Rent alone in metros eats 40–60% of the supposed "needs" bucket — before factoring food, utilities, transport, EMI, or insurance.

For most Indian metro earners, the realistic split is closer to 60–70% needs, 15% wants, 15–20% savings.

Adjusted ratios that work for Indian life

For metros (Mumbai / Bengaluru / Delhi) with rent > 30% of income

- 60% needs

- 20% wants

- 20% savings

Total still adds to 100%. The wants bucket shrinks; savings stays at the target 20%. Discipline shifts to lifestyle (fewer restaurants, fewer impulse buys) rather than housing (which is fixed-cost).

For Tier-2 cities with lower rent

- 50% needs

- 25% wants

- 25% savings

You have headroom. Raise the savings ratio — your future self will thank you. ₹12,500 / month invested at 12% for 25 years = ₹2.4 crore.

For starting careers (first 2-3 years, ₹25–40k income)

- 70% needs

- 20% wants

- 10% savings

Practical reality of fresher salaries. The 10% savings is non-negotiable — it builds the habit. Raise to 20% within 24 months as salary grows.

For high earners (₹2 L+ take-home)

- 35% needs

- 15% wants

- 50% savings

At high incomes, lifestyle inflation is the real enemy. Cap needs and wants in absolute ₹, route everything above into investments. This is how Indian wealth gets built — not from earning more, but from saving the increment.

How to actually run the rule (not just talk about it)

The rule fails when you mentally split your salary on the 1st and then spend without tracking. Three concrete habits to make it stick:

Habit 1 — Pre-commit on payday

The day your salary credits, set up standing instructions:

- Transfer 20% (or your target savings %) to a separate savings account / SIP

- Auto-pay rent + EMI on day 2

- What remains in your primary account is wants + variable needs

This is pay yourself first — the most reliable mechanism in personal finance.

Habit 2 — Track every transaction within 30 seconds

Wants budget runs out fastest. Without tracking, you'll discover the overspend on the 28th and feel ambushed. Tracking in real time tells you on the 18th, when you can still course-correct.

Money Track's Budgets module assigns each category to a 50/30/20 bucket and alerts when a bucket hits 80%. That single feature changes the rule from theory to lived habit.

The 50/30/20 Budget Calculator lets you adjust the ratios with sliders and see the rupee split — useful for setting realistic targets before you commit.

Habit 3 — Review once a month, not every day

Weekly tracking with monthly review beats daily anxiety. On the 1st of each month, look at last month's split:

- Did needs eat more than planned? What variable expense pushed it up?

- Did wants overshoot? Which category?

- Was savings actually saved, or did it leak into wants by the 25th?

One conversation with yourself, 10 minutes, monthly. That's enough.

What the rule gets right (even when ratios shift)

Even when the 50/30/20 percentages don't fit, three principles always hold:

- A category for guilt-free spending. Without this, you feel restricted, then binge, then feel guilty — the worst cycle in personal finance.

- A non-negotiable savings bucket that leaves your account before you can spend it. The percentage matters less than the act of automation.

- Distinguishing needs from wants in writing, not in your head. "Is Netflix a need?" is debatable until you've decided once and written it down.

What the rule gets wrong

It assumes housing is roughly 25–30% of income. In Indian metros, it's 35–50%. Don't beat yourself up for "failing" the rule — adjust the rule.

It treats EMI as needs. Home loan EMI principal repayment is actually wealth-building (you're paying yourself, building equity). Some advisers split EMI: interest portion → needs, principal portion → savings. Useful nuance for the disciplined.

It doesn't account for festivals + family obligations. Indian households often have ₹30–50k of "irregular obligation" expenses through the year (Diwali, weddings, parents' medical, gifts). Build a small monthly buffer (₹2–5k / month) so these don't crash your savings rate.

The shortest summary

- 50/30/20 is a starting point, not a target

- Adjust ratios to your reality: metros → 60/20/20; Tier-2 → 50/25/25; freshers → 70/20/10; high earners → 35/15/50

- The percentages matter less than the act of pre-committing savings and distinguishing needs from wants

- Track in real time, review monthly

- Build a buffer for festivals and family obligations so the rule doesn't break twice a year

Pick a ratio. Run it for 90 days. Adjust. Re-run. That's the entire method.